How much is auto insurance a month? This is a common question many people have.

The cost can vary based on different factors. Auto insurance is essential for every car owner. It protects you financially in case of an accident. But, how much should you expect to pay monthly? The answer depends on several things, like your driving history and the type of car you drive.

Other factors include your age, location, and coverage level. In this post, we will explore these factors in detail. Understanding them can help you estimate your monthly insurance cost. This way, you can budget better and find the best policy for your needs. Let’s dive into what affects your auto insurance rates each month.

Credit: www.policygenius.com

Introduction To Auto Insurance Costs

Auto insurance costs can be confusing. Many factors affect the monthly price. Understanding these can help you budget better and save money. Let’s dive into the basics of auto insurance costs.

Importance Of Auto Insurance

Auto insurance is crucial. It protects you financially in case of accidents. Without it, you might pay huge amounts from your pocket. This insurance covers damages to your car and others. It also handles medical costs if someone gets hurt. Having insurance is not just smart; it’s a legal requirement in many places.

Factors Influencing Costs

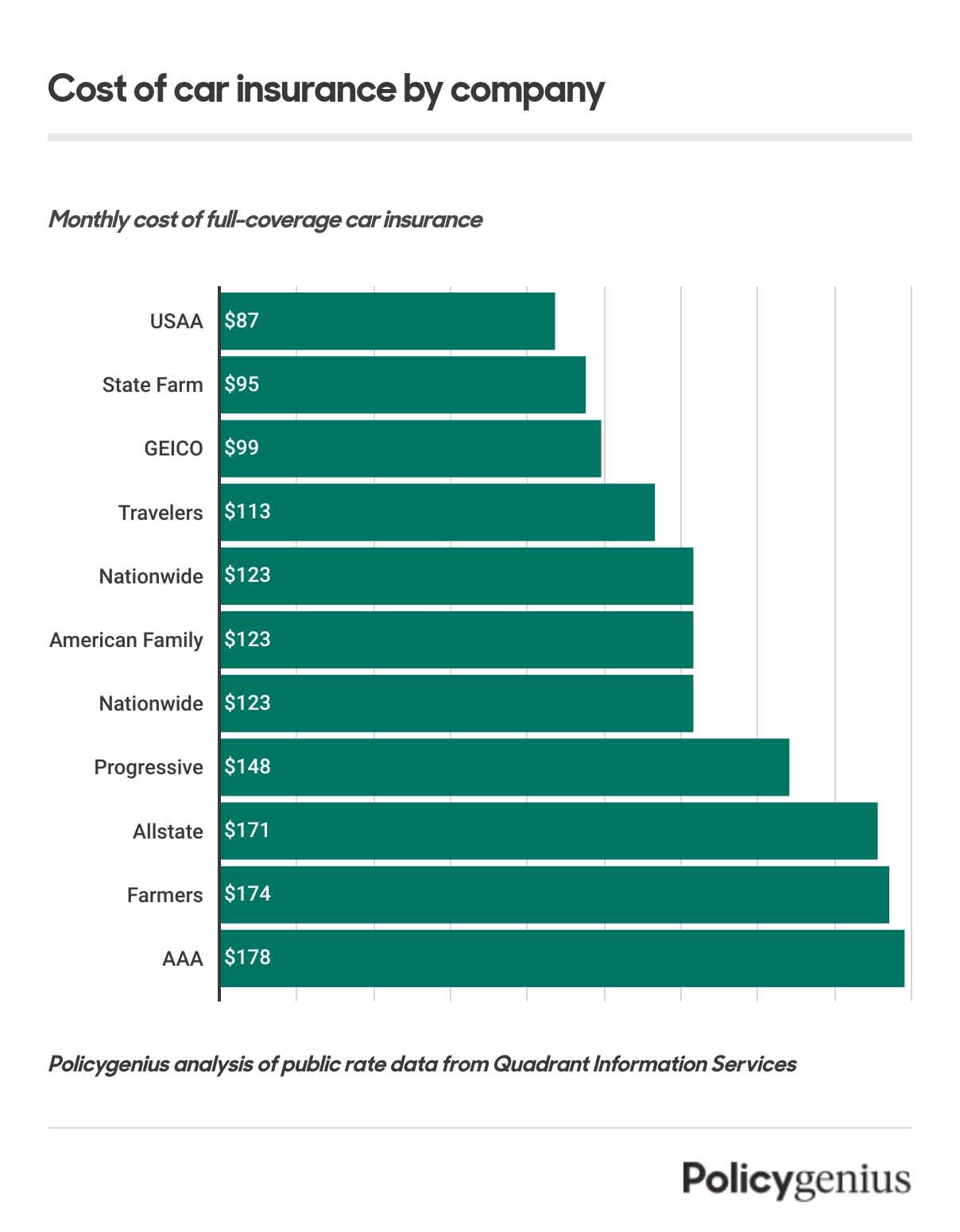

Several factors influence auto insurance costs. Your age and driving history matter. Younger drivers usually pay more. If you have accidents or tickets, your rates go up. The type of car you drive also affects the cost. Expensive cars cost more to insure. Where you live is another factor. City drivers often pay more due to higher accident rates. Your credit score can impact your insurance rate. Good credit can mean lower costs. The coverage levels you choose also play a role. More coverage means higher premiums. Lastly, some companies offer discounts. Safe driver discounts or bundling with other insurance can help lower costs.

Credit: www.insure.com

Average Monthly Rates

Understanding the average monthly rates for auto insurance can help you budget better. Costs vary based on several factors, including location, driving history, and coverage type. Let’s dive into the specifics of what you might expect to pay each month for auto insurance.

National Averages

On average, drivers in the United States pay about $120 per month for auto insurance. This figure reflects a mid-range policy with standard coverage. Premiums can be higher or lower depending on individual circumstances.

Most drivers spend between $100 and $150 monthly. High-risk drivers or those with luxury vehicles may see higher premiums. Discounts can reduce these rates, sometimes significantly.

State-by-state Variations

Auto insurance costs vary widely by state. For instance, drivers in Michigan often pay more than $200 per month. This is due to state-specific laws and higher coverage requirements.

In contrast, drivers in Maine might pay around $70 per month. States with fewer traffic accidents and lower crime rates tend to have cheaper insurance. Always check the specific rates for your state to get an accurate estimate.

Factors Affecting Premiums

Auto insurance premiums can vary widely based on several factors. Understanding these factors can help you estimate your monthly costs. Let’s dive into some of the key elements that affect your auto insurance rates.

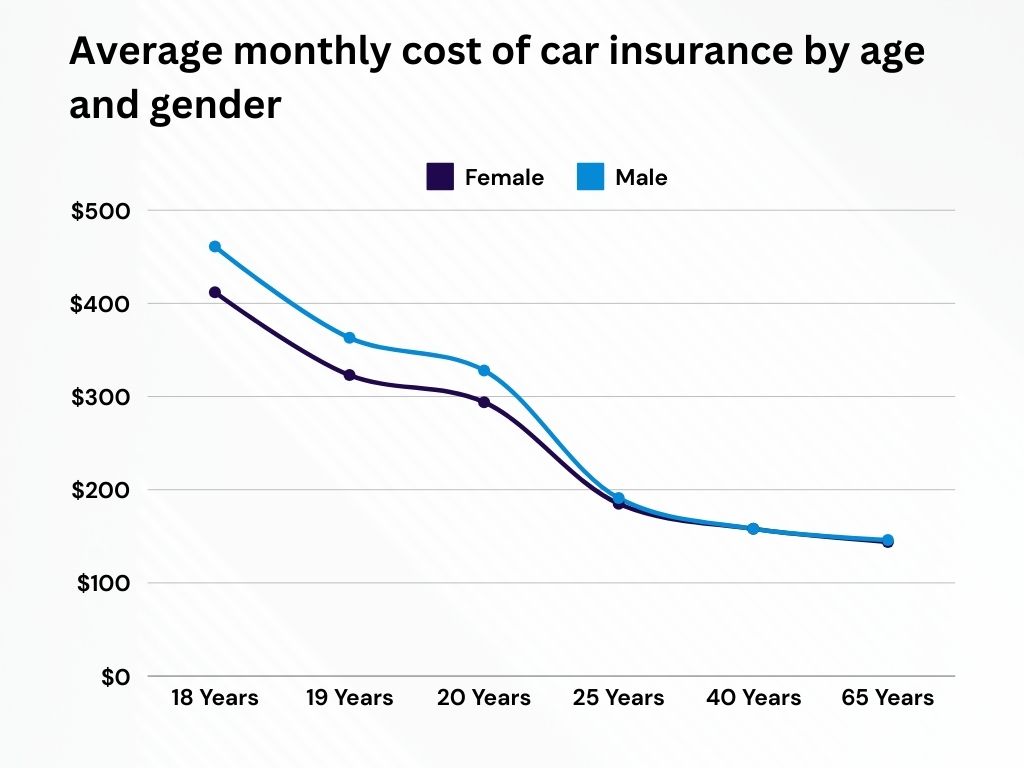

Driver’s Age And Experience

Insurance companies consider the driver’s age as a significant factor. Younger drivers often face higher premiums. This is due to their lack of driving experience. Teen drivers, for instance, are seen as high-risk. Conversely, older drivers with more experience usually pay lower rates. They are perceived as safer drivers.

Vehicle Type And Usage

The type of vehicle you drive also impacts your insurance premium. Sports cars typically cost more to insure. They are associated with higher speeds and more accidents. Family sedans, on the other hand, usually have lower premiums. They are considered safer and less likely to be involved in accidents.

How you use your vehicle matters too. Cars used for daily commuting may have higher premiums. This is because they are on the road more often. Vehicles used only occasionally might have lower rates. They pose a lower risk of accidents.

Impact Of Driving Record

Your driving record has a significant impact on your auto insurance rates. Insurance companies look at your past driving behavior to predict your future risk. A clean record can save you money. On the other hand, a history of accidents and violations can increase your premiums.

Accidents And Claims

Accidents can raise your insurance rates. The more severe the accident, the higher the increase. Even minor accidents may lead to higher premiums. Insurance companies see a pattern in frequent claims. They may label you as a high-risk driver. This can result in higher monthly payments.

Traffic Violations

Traffic violations also affect your insurance costs. Speeding tickets are a common example. They signal risky driving behavior to insurers. Each ticket can cause your rates to go up. More serious offenses like DUIs have a greater impact. They can lead to substantial rate hikes. Multiple violations can put you in a high-risk category. This makes it difficult to find affordable insurance.

Role Of Coverage Levels

The amount you pay for auto insurance each month depends on many factors. One key factor is the type of coverage you choose. Coverage levels play a crucial role in determining your premium. Below, we’ll dive into two main types of coverage: Liability Coverage and Comprehensive and Collision.

Liability Coverage

Liability coverage is the most basic form of auto insurance. It covers costs for damages and injuries you cause to others. There are two main components:

- Bodily Injury Liability: Pays for medical expenses and lost wages of the other party.

- Property Damage Liability: Covers the cost to repair damage to the other party’s property.

The higher your coverage limits, the higher your premium will be. But higher limits also offer greater protection. If you have significant assets, higher liability coverage is advisable.

Comprehensive And Collision

Comprehensive and collision coverage protect your own vehicle. They are more expensive but provide extensive protection.

Comprehensive Coverage: Covers non-collision events like theft, fire, and natural disasters. For example, if a tree falls on your car, comprehensive coverage will handle the repairs.

Collision Coverage: Covers damage to your car from collisions with other vehicles or objects. If you hit a pole, collision coverage will pay for the repairs to your car.

Both types of coverage come with a deductible. A higher deductible means a lower premium but more out-of-pocket costs if you file a claim.

Discounts And Savings

Understanding the cost of auto insurance can be daunting. But there are ways to reduce your monthly expenses. Discounts and savings can make a big difference in how much you pay. Let’s explore some common discounts available.

Safe Driver Discounts

Many insurance companies reward safe drivers. If you have a clean driving record, you may qualify for a safe driver discount. This means no accidents or traffic violations. Insurance companies see you as low risk. They often pass on the savings to you.

Some companies even use technology to track your driving habits. Good driving behavior can lead to lower rates. For example, driving within speed limits, avoiding sudden stops, and not using your phone while driving. These actions can help you save money each month.

Bundling Policies

Another way to save is by bundling policies. This means getting multiple insurance types from the same provider. For instance, you can bundle auto and home insurance. Many companies offer significant discounts for this.

Bundling can simplify your life. You deal with one company for multiple needs. It also often leads to a reduced overall premium. Below is an example table showing potential savings from bundling:

| Insurance Type | Individual Monthly Premium | Bundled Monthly Premium | Monthly Savings |

|---|---|---|---|

| Auto Insurance | $100 | $85 | $15 |

| Home Insurance | $80 | $70 | $10 |

| Total | $180 | $155 | $25 |

As shown, bundling can lead to significant savings. It’s worth exploring if you’re looking to cut costs on your auto insurance.

Comparison Shopping

Finding the right auto insurance can be challenging. Comparison shopping helps you get the best rates. By comparing different providers, you can save money and find the right coverage for your needs. This section explores the tools and resources for comparison shopping.

Online Tools And Resources

Online tools make comparison shopping easier. These tools allow you to compare rates from different providers. Some popular tools include:

- Insurance comparison websites: Websites like NerdWallet and The Zebra provide side-by-side comparisons.

- Company websites: Many insurers offer online quote tools.

- Mobile apps: Apps like Gabi and Jerry help you compare and manage insurance policies.

These tools save time and help you find the best deals. They also provide reviews and ratings from other customers, making it easier to choose the right provider.

Getting Multiple Quotes

Obtaining multiple quotes is essential for finding the best rate. You should aim to get at least three quotes from different insurers. This gives you a better idea of the market rates.

Here are some tips for getting multiple quotes:

- Prepare your information: Gather details about your car and driving history.

- Use online tools: Utilize comparison websites and apps to get quotes quickly.

- Contact agents: Speak with insurance agents to get personalized quotes.

By comparing multiple quotes, you can find the best coverage at the lowest price. This helps you make an informed decision and ensures you are not overpaying for your auto insurance.

Tips For Lowering Costs

Auto insurance can be expensive, but there are effective ways to reduce costs. Making small changes can lead to significant savings. Below are some practical tips for lowering auto insurance costs.

Improving Your Credit Score

Your credit score plays a vital role in determining your insurance premium. Insurers view a higher credit score as a sign of reliability. Improving your credit score can lower your insurance costs.

- Pay bills on time.

- Reduce outstanding debt.

- Check your credit report for errors.

Regularly monitor your credit score. Use credit monitoring tools to stay on top of your credit status. These steps can help you save money on auto insurance.

Choosing Higher Deductibles

Opting for a higher deductible can reduce your monthly insurance premium. A deductible is the amount you pay out of pocket before insurance kicks in. Higher deductibles mean lower premiums.

Consider the following deductible options:

| Deductible Amount | Average Monthly Premium |

|---|---|

| $250 | $150 |

| $500 | $120 |

| $1,000 | $90 |

Choose a deductible amount that fits your budget. Ensure you can afford the out-of-pocket cost in case of an accident. Weigh the savings on premiums against the potential expenses.

Credit: www.insure.com

Frequently Asked Questions

How Much Is Auto Insurance Monthly?

The cost of auto insurance varies by state, provider, and coverage. On average, it ranges from $100 to $200 per month. Your driving history and vehicle type can also affect the price.

What Factors Affect Auto Insurance Rates?

Several factors influence auto insurance rates. These include your age, driving record, location, vehicle type, and coverage level. Credit score and claims history also play a role.

Can I Lower My Auto Insurance Cost?

Yes, you can lower your auto insurance cost. Shop around for quotes, increase your deductible, and look for discounts. Maintaining a clean driving record helps too.

Is Full Coverage Auto Insurance Necessary?

Full coverage may not be necessary for everyone. It is advisable if you have a new or high-value car. Liability coverage is the minimum required by law.

Conclusion

Auto insurance costs vary each month. Factors like age and vehicle type matter. Comparing quotes helps you find the best rate. Always review your coverage options. This ensures you get the protection you need. Remember, cheap isn’t always best. Focus on value and coverage.

Understanding your policy helps avoid surprises. Regularly check for discounts. Stay informed and save money. Your peace of mind is priceless. Choose wisely and drive safely.